National Bank Financial, 24 November 2006

Excerpt from the report titled 'Canadian Banks - Q4 2006 Quarterly: New '08 EPS Estimates; Still Very Bullish," 21 November 2006

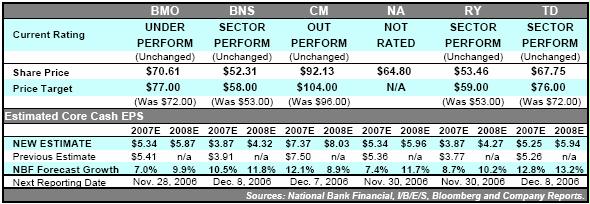

• Still very bullish: F2006 has been a solid year for the banks. Benefiting from a favourable operating environment, and with lending NII, very promisingly, showing signs of improvement, the banks continue to report strong EPS growth. This fact, combined with (still) attractive valuations, low risk, and most importantly, our expectation of another 2 years of double-digit EPS growth, supports our continued bullish stance (although a short-term correction is possible).

• Introducing F2008 estimates (and updating F2007): We are revising our F2007 estimates and introducing F2008 forecasts, which assume Y/Y growth of 9.8% and 10.9% respectively. Our investment thesis for the next 2 years incorporates (i) increases in PCLs of over 20% per year, (ii) a modest recovery in net CMRR from lower F2006 levels, (iii) good loan growth & modestly improving margins, and (iv) a large decline in securities gains.

• A powerful earnings driver reawakens: Last quarter, much higher lending NII, supported by solid loan growth and margin expansion, helped drive the excellent 14% Y/Y EPS growth. Over the next 2 years, we expect lending NII to take over from provisions as the primary driver of double-digit earnings growth.

• Will tax on Income Trusts drive higher payout ratios? Although capital deployment continues to be the most important secular trend facing the banks, dividend growth also remains important. In our view, the tax on income trusts and investors' heightened demand for yield may cause the three banks (BNS, NA, TD) with the lowest payout ratios (35% to 45%) to increase their target ranges, supporting already solid dividend growth for the sector.

• Conclusion - solid growth prospects support bullish stance: The group's fundamentals remains robust, with high ROEs, strong capital, and double-digit EPS growth expected. As of November 17th, the group traded at 13.0x and 11.7x our F2007 and F2008 estimates respectively, levels we believe to be attractive given the sector's (higher) growth and (low) risk profile. Our top pick is CM.

Excerpt from the report titled 'Canadian Banks - Q4 2006 Quarterly: New '08 EPS Estimates; Still Very Bullish," 21 November 2006

• Still very bullish: F2006 has been a solid year for the banks. Benefiting from a favourable operating environment, and with lending NII, very promisingly, showing signs of improvement, the banks continue to report strong EPS growth. This fact, combined with (still) attractive valuations, low risk, and most importantly, our expectation of another 2 years of double-digit EPS growth, supports our continued bullish stance (although a short-term correction is possible).

• Introducing F2008 estimates (and updating F2007): We are revising our F2007 estimates and introducing F2008 forecasts, which assume Y/Y growth of 9.8% and 10.9% respectively. Our investment thesis for the next 2 years incorporates (i) increases in PCLs of over 20% per year, (ii) a modest recovery in net CMRR from lower F2006 levels, (iii) good loan growth & modestly improving margins, and (iv) a large decline in securities gains.

• A powerful earnings driver reawakens: Last quarter, much higher lending NII, supported by solid loan growth and margin expansion, helped drive the excellent 14% Y/Y EPS growth. Over the next 2 years, we expect lending NII to take over from provisions as the primary driver of double-digit earnings growth.

• Will tax on Income Trusts drive higher payout ratios? Although capital deployment continues to be the most important secular trend facing the banks, dividend growth also remains important. In our view, the tax on income trusts and investors' heightened demand for yield may cause the three banks (BNS, NA, TD) with the lowest payout ratios (35% to 45%) to increase their target ranges, supporting already solid dividend growth for the sector.

• Conclusion - solid growth prospects support bullish stance: The group's fundamentals remains robust, with high ROEs, strong capital, and double-digit EPS growth expected. As of November 17th, the group traded at 13.0x and 11.7x our F2007 and F2008 estimates respectively, levels we believe to be attractive given the sector's (higher) growth and (low) risk profile. Our top pick is CM.

__________________________________________________________

The Globe and Mail, Roma Luciw, 24 November 2006

Canada's biggest banks are expected to report higher year-over-year profit when they start releasing results next week, but earnings growth could slow from the previous quarter as the credit cycle darkens.

“We believe credit quality and equity markets are unlikely to be as good for the banks in upcoming years as in the last five years,” said Merrill Lynch analyst Andre-Philippe Hardy.

Fourth-quarter core profit among the six largest Canadian banks is expected to rise 12 per cent from last year. Merrill is looking for Royal Bank of Canada to lead the way on “easy reinsurance comparisons” while CIBC is likely to come in at the low end, “mainly driven by lower merchant banking gains,” Mr. Hardy said.

Compared with the third quarter, he expects per share profit will drop 2 per cent on a 25 per cent projected rise in provisions for credit losses. “We believe new provision levels remained low in both personal and corporate lending as credit conditions remain benign,” Mr. Hardy said.

Strong capital markets were stronger-than-expected in October, he said. Strong debt underwriting, mergers and acquisition advisory fees and wealth management sales will be partially be offset by lower equity underwriting revenues and flat to lower trading revenues.

Bank of Montreal will be the first of the big six to report earnings on Nov. 28, followed by Royal Bank of Canada and National Bank on Nov. 30, Canadian Imperial Bank of Commerce on Dec. 7, Toronto-Dominion Bank and Bank of Nova Scotia on Dec. 8.

The S&P/TSX capped financial sub-index has risen 14 per cent so far this year, outperforming a 12.2 per cent gain by the S&P/TSX composite index.

Although lower bond yields, higher capitalization levels, decreased exposure to credit risk, and lower personal dividend tax rates have boosted the bank's multiples, Mr. Hardy does not believe the credit or equity market environment will be as positive for the big banks in the coming years.

“We do not believe further expansion is likely given our outlook for slowing earnings growth,” he said.

Robert Wessel, the banking analyst for National Bank Financial Inc., forecasts bank profits will increase 9.8 per cent in 2007 and 10.9 per cent in 2008 and trade at 13 times and 11.7 times, respectively, his profit estimates.

James Keating, an analyst with RBC Dominion Securities Inc. is looking for about a 13-per-cent return, including dividends, from the banks.

Canada's biggest banks are expected to report higher year-over-year profit when they start releasing results next week, but earnings growth could slow from the previous quarter as the credit cycle darkens.

“We believe credit quality and equity markets are unlikely to be as good for the banks in upcoming years as in the last five years,” said Merrill Lynch analyst Andre-Philippe Hardy.

Fourth-quarter core profit among the six largest Canadian banks is expected to rise 12 per cent from last year. Merrill is looking for Royal Bank of Canada to lead the way on “easy reinsurance comparisons” while CIBC is likely to come in at the low end, “mainly driven by lower merchant banking gains,” Mr. Hardy said.

Compared with the third quarter, he expects per share profit will drop 2 per cent on a 25 per cent projected rise in provisions for credit losses. “We believe new provision levels remained low in both personal and corporate lending as credit conditions remain benign,” Mr. Hardy said.

Strong capital markets were stronger-than-expected in October, he said. Strong debt underwriting, mergers and acquisition advisory fees and wealth management sales will be partially be offset by lower equity underwriting revenues and flat to lower trading revenues.

Bank of Montreal will be the first of the big six to report earnings on Nov. 28, followed by Royal Bank of Canada and National Bank on Nov. 30, Canadian Imperial Bank of Commerce on Dec. 7, Toronto-Dominion Bank and Bank of Nova Scotia on Dec. 8.

The S&P/TSX capped financial sub-index has risen 14 per cent so far this year, outperforming a 12.2 per cent gain by the S&P/TSX composite index.

Although lower bond yields, higher capitalization levels, decreased exposure to credit risk, and lower personal dividend tax rates have boosted the bank's multiples, Mr. Hardy does not believe the credit or equity market environment will be as positive for the big banks in the coming years.

“We do not believe further expansion is likely given our outlook for slowing earnings growth,” he said.

Robert Wessel, the banking analyst for National Bank Financial Inc., forecasts bank profits will increase 9.8 per cent in 2007 and 10.9 per cent in 2008 and trade at 13 times and 11.7 times, respectively, his profit estimates.

James Keating, an analyst with RBC Dominion Securities Inc. is looking for about a 13-per-cent return, including dividends, from the banks.

__________________________________________________________

The Globe and Mail, Allan Robinson, 24 November 2006

The banks begin reporting their fourth-quarter results next week, led by Bank of Montreal on Tuesday, and the group will need to play a pivotal role if the S&P/TSX composite index is to continue to climb next year.

"I will point out that while the S&P/TSX return will be fairly good, you are looking at a polarized stock market, with most of the return expected from two sectors, energy and financials," said Jeff Rubin, chief strategist for CIBC World Markets Inc.

That could be good news. "The TSX seems made to order for an environment of rising energy prices and falling interest rates," Mr. Rubin said. Two-thirds of the market capitalization of companies comprising the index are in interest-sensitive and energy stocks.

CIBC has a 12-month target for the index of S&P/TSX of 13,500, which implies the market could move up another 7 per cent from its close yesterday at 12,644.9. Since Nov. 1, the index has surged 4.9 per cent.

Investors in bonds and stocks are anticipating the U.S. Federal Reserve Board and the Bank of Canada could begin cutting interest rates next year, strategists say.

"The banks have historically been the major beneficiaries of interest rate decline," Mr. Rubin said. Relatively high-yielding utilities and telecom stocks also benefit, he said. The banking sector currently yields about 3.1 per cent.

CIBC estimates that for every 100 basis points cut in 10-year yields, the share price of banks increase on average by about 9.5 per cent. The yield on 10-year Canadian government bonds is currently 3.97 per cent and CIBC forecasts the yield could drop 55 basis points to 60 points next year, which implies more than a 5-per-cent gain in the bank shares from that alone. (A basis point is 1/100th of a percentage point.) The bank shares could also get a boost from rising profits, which CIBC estimates will increase 14 per cent in the fourth quarter and 12 per cent during 2007, Mr. Rubin said. Lower interest rates boost profit margins and lower default rates.

James Keating, an analyst with RBC Dominion Securities Inc. is looking for about a 13-per-cent return, including dividends, from the banks. On a year-to-date basis, the banks have outperformed the S&P/TSX by 3.3 percentage points after rising 14 per cent during the past four months, he said. Robert Wessel, the banking analyst for National Bank Financial Inc., forecasts bank profits will increase 9.8 per cent in 2007 and 10.9 per cent in 2008 and trade at 13 times and 11.7 times, respectively, his profit estimates. He remains bullish.

The banks begin reporting their fourth-quarter results next week, led by Bank of Montreal on Tuesday, and the group will need to play a pivotal role if the S&P/TSX composite index is to continue to climb next year.

"I will point out that while the S&P/TSX return will be fairly good, you are looking at a polarized stock market, with most of the return expected from two sectors, energy and financials," said Jeff Rubin, chief strategist for CIBC World Markets Inc.

That could be good news. "The TSX seems made to order for an environment of rising energy prices and falling interest rates," Mr. Rubin said. Two-thirds of the market capitalization of companies comprising the index are in interest-sensitive and energy stocks.

CIBC has a 12-month target for the index of S&P/TSX of 13,500, which implies the market could move up another 7 per cent from its close yesterday at 12,644.9. Since Nov. 1, the index has surged 4.9 per cent.

Investors in bonds and stocks are anticipating the U.S. Federal Reserve Board and the Bank of Canada could begin cutting interest rates next year, strategists say.

"The banks have historically been the major beneficiaries of interest rate decline," Mr. Rubin said. Relatively high-yielding utilities and telecom stocks also benefit, he said. The banking sector currently yields about 3.1 per cent.

CIBC estimates that for every 100 basis points cut in 10-year yields, the share price of banks increase on average by about 9.5 per cent. The yield on 10-year Canadian government bonds is currently 3.97 per cent and CIBC forecasts the yield could drop 55 basis points to 60 points next year, which implies more than a 5-per-cent gain in the bank shares from that alone. (A basis point is 1/100th of a percentage point.) The bank shares could also get a boost from rising profits, which CIBC estimates will increase 14 per cent in the fourth quarter and 12 per cent during 2007, Mr. Rubin said. Lower interest rates boost profit margins and lower default rates.

James Keating, an analyst with RBC Dominion Securities Inc. is looking for about a 13-per-cent return, including dividends, from the banks. On a year-to-date basis, the banks have outperformed the S&P/TSX by 3.3 percentage points after rising 14 per cent during the past four months, he said. Robert Wessel, the banking analyst for National Bank Financial Inc., forecasts bank profits will increase 9.8 per cent in 2007 and 10.9 per cent in 2008 and trade at 13 times and 11.7 times, respectively, his profit estimates. He remains bullish.

__________________________________________________________

The Globe and Mail, 24 November 2006

James Keating, an analyst with RBC Dominion Securities Inc., rates the Toronto-Dominion Bank as an "outperform" and says the decision to take 40-per-cent-owned TD Banknorth private is a turning point.

Yesterday, he raised his share profit forecasts on a cash basis by 4 cents in 2007 and 5 cents in 2008 to $5.40 and $6.05, respectively. Mr. Keating describes his profit increase as a "tweak," but he says RBC's cash estimate is the highest on the Street.

"In our view, investors are too bearish on TD's earnings-per-share outlook, meaning the discounted price-to-earnings multiple is doubly attractive."

The latest deal simplifies the corporate structure, adds to future profit and increases the incremental leverage to any rise in the U.S.-Canadian dollar exchange rate, he said.

The shares of the bank closed yesterday at $67.96, up 55 cents. RBC's 12-month share price target is $84.

;

James Keating, an analyst with RBC Dominion Securities Inc., rates the Toronto-Dominion Bank as an "outperform" and says the decision to take 40-per-cent-owned TD Banknorth private is a turning point.

Yesterday, he raised his share profit forecasts on a cash basis by 4 cents in 2007 and 5 cents in 2008 to $5.40 and $6.05, respectively. Mr. Keating describes his profit increase as a "tweak," but he says RBC's cash estimate is the highest on the Street.

"In our view, investors are too bearish on TD's earnings-per-share outlook, meaning the discounted price-to-earnings multiple is doubly attractive."

The latest deal simplifies the corporate structure, adds to future profit and increases the incremental leverage to any rise in the U.S.-Canadian dollar exchange rate, he said.

The shares of the bank closed yesterday at $67.96, up 55 cents. RBC's 12-month share price target is $84.